- WeekendInvesting

- Posts

- What?! Its the 2nd Biggest Fall in Nifty ?

What?! Its the 2nd Biggest Fall in Nifty ?

What's the Sign of Worry?

WeekendInvesting Analytics

March 13, 2026

We are thrilled to let you know that we have opened 25 slots for the HNI Strategies !

Know More : https://youtu.be/gsGCc6cssyM

Click on the button below to request for performance

Note : We have opened only 25 slots (on first come first serve basis)

Market Update - Friday, 13 Mar

The day and the date itself seemed indicative of the market sentiment, and unfortunately, the worst fears came true as markets collapsed like nine pins.

Looking at the historical data of the ten worst monthly returns over the last decade, March 2020 remains the steepest drop at 23% due to the Covid-19 pandemic. However, March 2026 is already ranking as the second-worst month of the last ten years, and the month is not even halfway through. This reflects the intense pain the market is currently bearing, and it is difficult to predict where levels will settle by the end of the month.

In times like these, there are essentially two ways to react. One is to succumb to fear and decide the market is no longer worth the risk. The other is to learn from history and recognize that one should stay the course. It is vital to stick to a predefined plan.

The market charts show a completely demolished landscape, with an additional 2% drop today. While there is hope that a bottom is near, technical supports appear closer to the 22,000 mark, which is still a thousand points away.

A trend reversal likely depends on a resolution of the current oil situation, which remains the most damaging factor. As days pass, oil storage may begin to run out, creating further complications. Currently, there are no clear signals on the chart of an immediate turnaround.

Nifty Junior was smashed down 2.61%, hitting a new low for the year.

Mid-caps and small-caps both fell by 2.6%, while Bank Nifty dropped 2.44%. This is a complete bloodbath with no pockets of safety.

Even gold and silver are feeling a liquidity crunch; gold is priced at 16,036 and may dip further in the short term, while silver fell 0.98% to 2,61,682.

Other Market Triggers

Heavyweights faced significant losses, including Axis Bank, SBI, Maruti, Mahindra, Eicher, and L&T, which dropped 7.5%.

Steel and cement stocks like JSW Steel, UltraTech, Tata Steel, and Hindalco were also hit hard.

Only Bharti Airtel, Tata Motors, Tata Consumer, and Hindustan Unilever managed to sustain their positions.

The Nifty Next 50 heatmap was entirely red, signaling a day of capitulation where investors seem to be giving up.

In the mover of the day segment, IFCI rose 6% on news that the NSE is appointing legal advisors and bankers for an IPO, as IFCI holds a large stake in the exchange.

Zydus Wellness saw an intraday zoom due to insider and promoter buying before giving up most gains to close around 412.

U.S. Market Updates

The US markets also saw a weak session, with the S&P 500, Dow Jones, and Nasdaq losing over 1.5%.

Big names like Intel, GE, and Goldman Sachs lost between 4.5% and 5.5%.

What to watch next ?

A key concern highlighted by Nomura is the energy exposure of Asian countries to the Strait of Hormuz. India is 93% dependent on fossil fuels and 40% of its energy imports come from the Middle East.

This highlights the urgent need for true self-reliance in energy and mineral exploration, as the current 25-day reserves offer a limited buffer.

The market remains extremely dependent on a de-escalation of conflict and the reopening of the Strait of Hormuz for shipping vessels.

While the stress may not vanish instantly, such news would likely see it dissipate rapidly.

Get your Portfolio Momentum Report today and ensure your investments are positioned for success!

Forwarded this email? Subscribe Now

Top Trending Strategies

Mi EverGreenPower of Gold with Equity | Allocate 20 strongest CNX200 stocks with Gold ETF | Monthly Rebalanced Mi Evergreen is a dynamic strategy which aims to outperform the underlying benchmark CNX200. This index comprises 200 large and mid-cap names which are the top-quality stocks in the markets. This product is suitable for use in all stages of the market cycles as it is designed to invest in the strongest stocks in the pack at any point. Additionally, there is a permanent hedge of Gold available here.

| Mi AllCap GOLDA core strategy to allocate 25% each to Large Cap , Mid Caps, Small Caps & Gold Mi AllCap GOLD is a robust, rule-based core rotational strategy from the House of WeekendInvesting, curated to cover stocks in the CNX500 universe, designed to offer a balanced asset allocation and diversified wealth creation approach for compounding returns over long periods of time.

|

The Silent Thief: Why Your "Safe" Savings are Shrinking

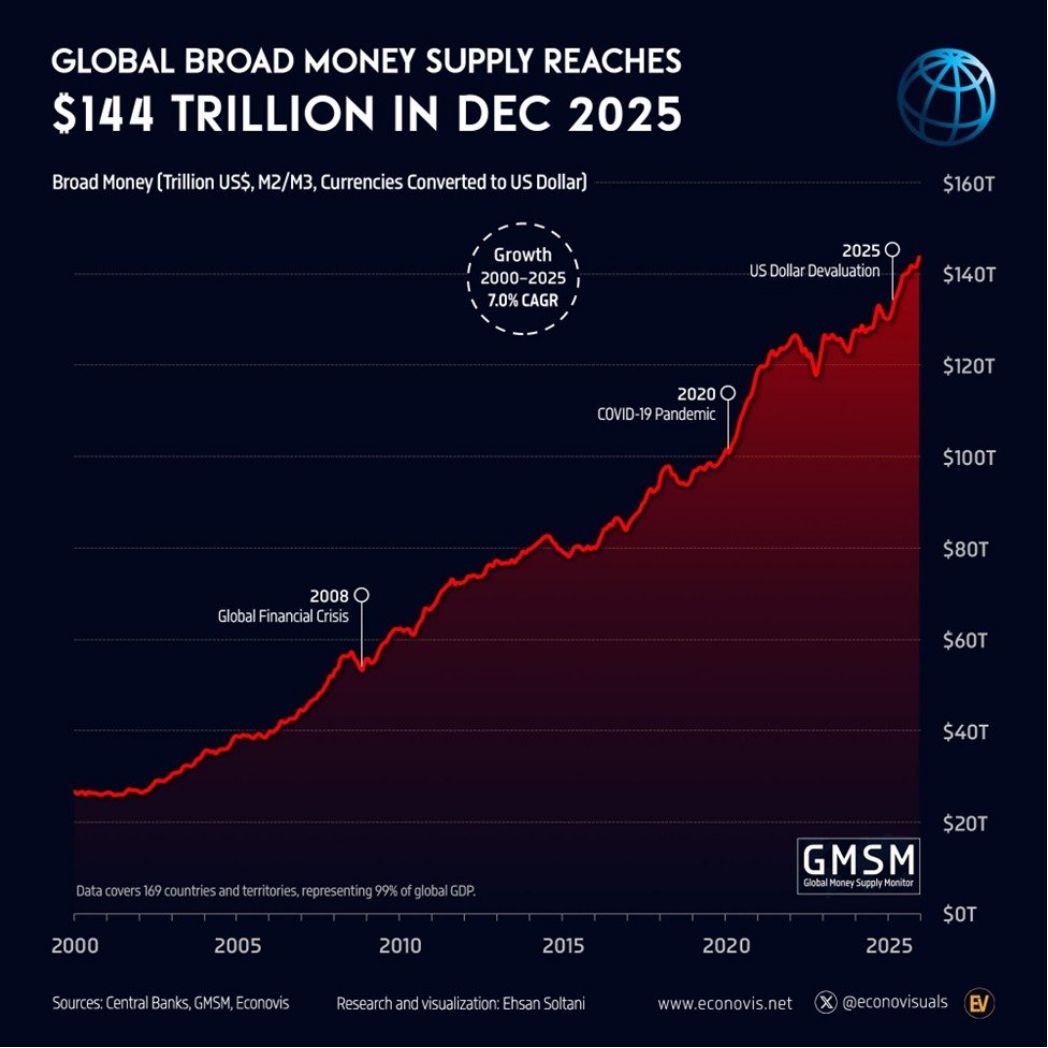

Recent data from the kobeissi Letter highlights a startling trend: the global broad money supply is expanding at a rate of 10.4% year-on-year.

Source : The Kobeissi Letter on X

Whether it is physical printing or digital creation, the "money base" is ballooning. While more money in the system sounds good in theory, it fundamentally changes the math of your wealth.

The Arithmetic of Wealth Erosion

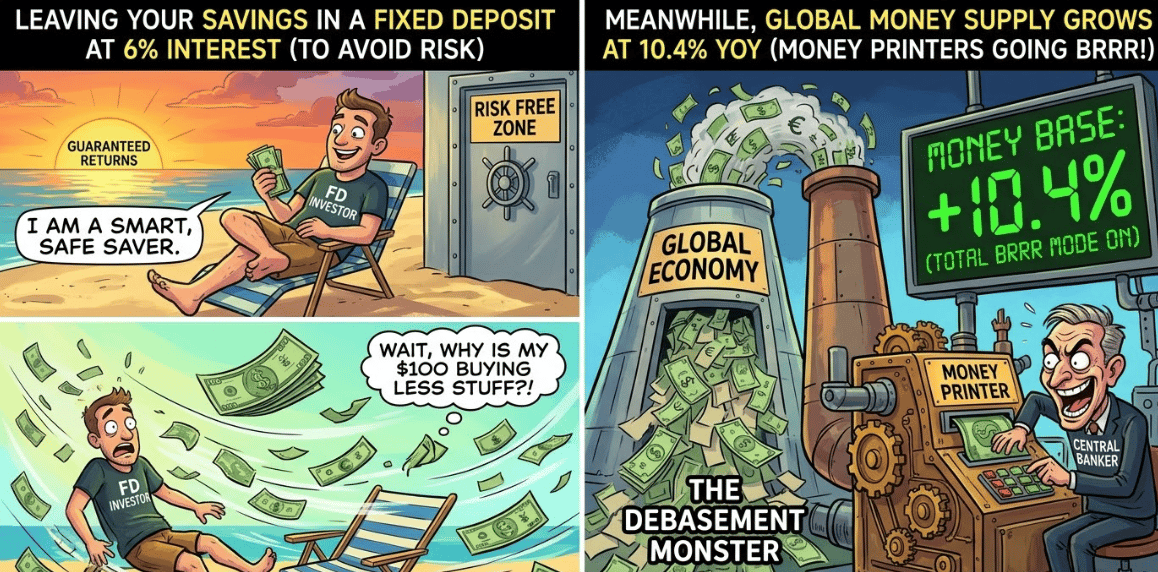

Economics is a game of supply and demand. When the supply of money increases by double digits, the purchasing power of each individual unit drops. If the money supply grows by over 10% but your assets—like a standard Fixed Deposit (FD)—are only yielding 6% or 7%, you aren't "earning" 6%. In reality, you are losing roughly 4% of your wealth's value every single year. You are effectively working harder to stay in the same place.

The Escape Hatch: Scarcity is King

To protect yourself from the "debasement" of currency, you must pivot toward Real Assets. These are things that cannot be printed out of thin air. When money becomes "cheap," items with limited supply become "expensive."

To outpace the 10.4% money growth, consider diversifying into:

Equities: Quality stocks that grow with the economy.

Hard Assets: Real Estate and Gold (which has historically averaged 13-14% returns over the long term).

Alternative Stores of Value: Antiques, collectibles, or any asset defined by scarcity.

Rethinking Risk: The Danger of Doing Nothing

Many investors avoid the stock market because it feels "dangerous." However, the data suggests that avoiding risk is the biggest risk of all. If you stay 100% in cash or low-interest bank accounts, you are guaranteed to lose value over time. Even a conservative split—perhaps 20% in stocks and 80% in banks—can provide a necessary buffer against the inflation caused by an expanding money supply.

Meme Of The Day

The global money supply is growing at 10.4% annually, but traditional "safe" savings are only giving us 6-7%. Knowing this, how are you adjusting your strategy? |

|

Share this daily insightful newsletter with your market savvy friends and family or sign them up for the newsletter !

For detailed blogs, reports and strategies, check WeekendInvesting.com

Reply